Of the many tax-deductible investments, oil investment tax breaks offer numerous advantages unique to the industry such as the tax treatment of intangible drilling costs which are 100% deductible. Learn more about the tax benefits of oil and gas investments for the 2025 tax year.

Tax Deductible Investments

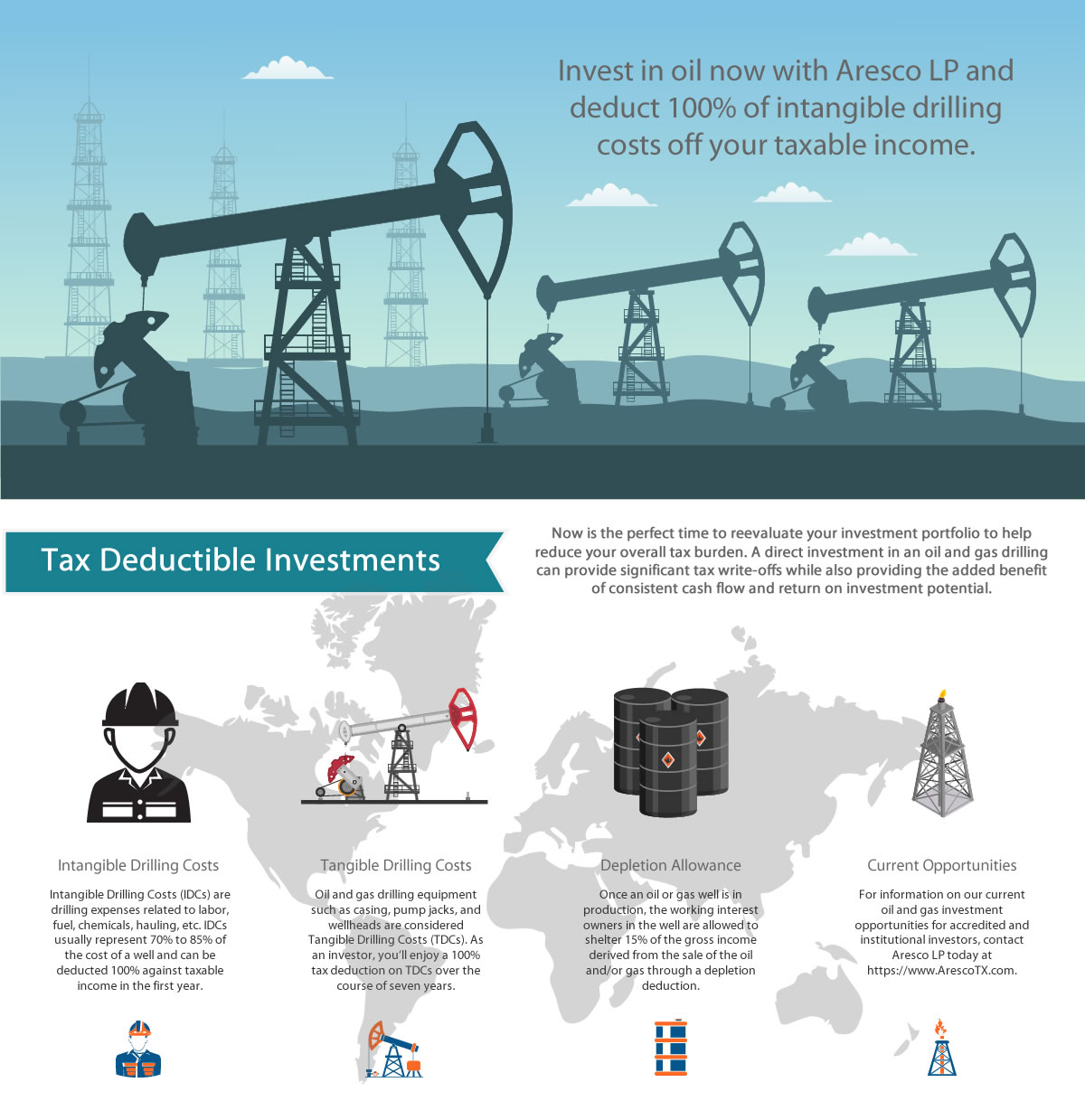

Now is the perfect time to reevaluate your investment portfolio to help reduce your overall tax burden. A direct investment in an oil and gas drilling partnership can provide significant tax write-offs while also providing the added benefit of consistent cash flow and return on investment potential.

100% Tax Deductible Investments

Oil Investing Tax Breaks – Invest in oil and deduct 100% of intangible drilling costs from your taxable income for 2025.

Instead of paying more to Uncle Sam, put more of your money to work instead.

Intangible Drilling Costs Tax Treatment

100% Tax Write Off of Intangible Drilling Costs (IDC) with a Direct Investment in Oil & Gas

Intangible Drilling Costs (IDCs) are drilling expenses related to labor, fuel, chemicals, hauling, etc. IDCs usually represent 70% to 85% of the cost of a well and can be deducted 100% against taxable income in the first year. For example, if you invested $50,000 today in a project that had 80% of its costs in IDCs, you could elect to deduct $40,000 from your taxable income for 2025. If you are in the top 37% federal tax bracket this deduction could save you approximately $14,800 in federal income taxes – please speak with your tax advisor for information specific to your situation.

IDC deductions are available in the year the money was invested, even if the well does not start drilling until March 31st of the year following the contribution of capital. Aresco has immediate oil investing drilling opportunities for 2025 tax deductions.

REQUEST MORE INFO BY FILLING OUT THE FORM >>

Oil Drilling Tax Deductions

Other Direct Oil Investing Tax Deductions & Tax Benefits

Tangible Drilling Costs – Capitalized and depreciated over a 7-year period

Oil and gas drilling equipment such as casing, pump jacks, and wellheads are considered Tangible Drilling Costs (TDCs). Continuing with the example above, the remaining $10,000 (20% of the cost of the well) would be classified as TDCs.

Intangible Completion Costs – Deductible in the year they are incurred

Intangible Completion Costs are generally related to non-salvageable goods and services, such as labor, completion materials, completion rig time, fluids etc. ICCs usually amount to about 15% of the total well cost and provide a great tax benefit.

Depreciation of Oil and Gas Assets – Depreciated over a 7-year period

Depreciation of Oil and Gas Assets – Depreciated over a 7-year period

While services and materials used during the drilling process offer no salvage value, equipment used in the completion and production of a well is generally salvageable. Items such as these are usually depreciated over a seven-year period, utilizing the Modified Accelerated Cost Recovery system or MACRS. Equipment in this category includes casing, tanks, wellhead and tree, pumping units, etc. Equipment and tangible completion expenses generally account for 15% to 30% of the total well cost.

Oil and Gas Depletion Allowance – Shelter 15% of the well’s annual production from income tax

Once an oil or gas well is in production, the working interest owners in the well are allowed to shelter some of the gross income derived from the sale of the oil and/or gas through a depletion deduction. Two types of depletion are available, cost and statutory (also referred to as percentage depletion). Cost depletion is calculated on the relationship between current production as a percentage of total recoverable reserves. Statutory or percentage depletion is subject to several qualifications and limitations. This deduction will generally shelter 15% of the well’s annual production from income tax.

REQUEST MORE INFO BY FILLING OUT THE FORM >>

Lease Operating Expense Oil and Gas – Tax Deductible in the year they are incurred without AMT consequences

Lease Operating Expenses cover the day-to-day costs involved with the operation of a well. The expense also covers the costs of re-entry or re-work of an existing producing well.

Lastly, the tax benefits from oil and natural gas production have historically triggered potential taxation under the Alternative Minimum Tax (AMT). However, Congress provided some tax relief in the early 1990s for “independent producers”. An independent producer was defined as an individual or company with production of 1,000 barrels per day or less. Although there is still the potential for AMT taxation for excess IDCs, percentage or statutory depletion is no longer considered a preference item.

Lastly, the tax benefits from oil and natural gas production have historically triggered potential taxation under the Alternative Minimum Tax (AMT). However, Congress provided some tax relief in the early 1990s for “independent producers”. An independent producer was defined as an individual or company with production of 1,000 barrels per day or less. Although there is still the potential for AMT taxation for excess IDCs, percentage or statutory depletion is no longer considered a preference item.

Click to Enlarge

Hydrocarbon Demand is Not Going Away

Despite the push for green energy and electric cars, the global demand of hydrocarbons is not going away. Did you know that hydrocarbons are used in the production of everyday items such as shampoo and lipstick? As a matter of fact, “green energy” would not even be possible without hydrocarbons. They are necessary for the manufacturing of solar panels as well as in the production and operation of wind turbines. The oil and gas industry will undoubtedly be a source of tax deductible investments for a very long time.

Disclaimer

The above general discussion is provided for background information only. This information is not intended to be individual advice. Prospective participants should consult with their personal tax professional regarding the applicability and effect of any and all benefits for their own personal tax situation. In addition, tax laws change from time to time and there is no guarantee regarding the interpretation of any tax laws regarding tax-deductible investments. Oil and gas tax deductions 2025 did not change significantly from oil and gas tax deductions 2024. For more information, please visit www.irs.gov.